Is Investment Management Front Office, Middle Office or Back Office?

What is Investment Management?

If you want to get a job in Investment Management, Banking, Hedge Fund, etc., you'll need to have a good understanding of front to back office structure and how they interrelate. As well as complex finance concepts and how they affect portfolio valuation.

To answer the question we must first explain some concepts.

What is investment?

To better understand investment management, it is important to know what investment really means. The best way to define investment is to explain it at its basic core. Investment is the act of deferring consumption. If you think about it, when you delay eating till later, you derive greater satisfaction when you do eat eventually. That greater satisfaction is equivalent to greater value of your deferred consumption.

So investment can be defined as the deliberate postponement of consumption in order to gain greater satisfaction (value) in future. The aim of investment is to gain greater value over time.

Investment also means a purposeful dedication to a cause. For instance, you can invest time to improve yourself by attending a self-development training, or to nurture a relationship (personal or business) by dedicating time to it. The aim is to grow it, improve it, and always strive to derive greater satisfaction (optimal value) from it as quickly as possible.

Most people associate investment with money. In this case, you save money in a bank account with the intention of earning future interest. By the time you get your money back from the bank, it should be worth more than what you put in. Note the word worth.

If you put in USD100 and after one year you get USD110, you've earned 10% over one year. But the question to answer is whether or not USD110 today can buy you more than what USD100 could have bought you a year ago. This is called Time Value of Money and it is used to measure the worth of money or investments, in real terms. It suggests that money is worth more now that in the future because of its potential earning capacity now (or opportunity cost). Therefore, the sooner you receive your money or interest, the better. In practical terms, this means that a bank account that will pay you interest four times a year or twice a year, is better than the one that will pay you interest once a year.

If your USD110 today buys you what USD100 would have bought you last year, then in real terms you haven't really gained USD10. Correct? This means that your USD110 today is actually worth less than what it seems. This is because of inflation - the general increase in the price of goods and services causing a fall in the real purchasing power (value) of money.

From the above example, we can conclude that inflation is 10% and you haven't increased the value of your money. Therefore, leaving your money in the bank is not an efficient way of investing. You need to look for a better way to save and quickly double your money, get above inflation return and optimise value.

What is the Rule of 72?

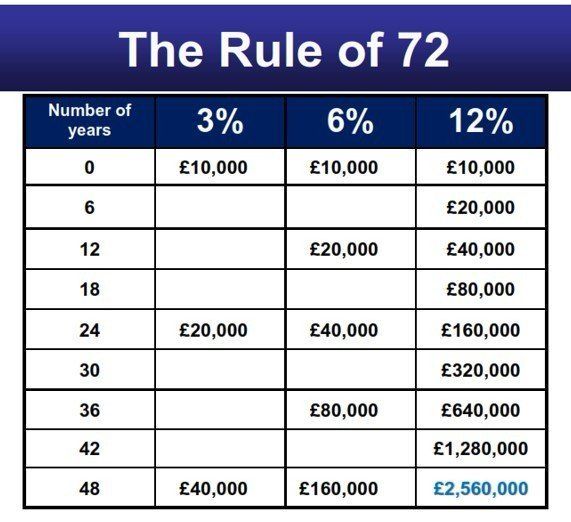

There are certain factors that indicate how best to manage money. We've considered two of them above - interest rate and inflation rate. Another one is the Rule of 72. It basically answers the question - how long will it take to double my money? If you divide 72 by the interest rate you are getting, it estimates how long it will take to double your money. From the above example, the interest rate was 10%. 72/10 = 7.2 years. That's how long it will take to grow the USD 100 to USD 200 in the bank at 10% interest rate. Think about these examples.

Active money management in terms of investment to optimise value requires mastery of financial management principles and use of complex algorithms to estimate future value and pay date. That's where investment management comes in.

What is investment management?

Investment management is basically the professional management

of financial securities (assets and liabilities) and other hard assets like property portfolios, shares and other investment certificates, etc., to optimise their marketable value and extract the maximum possible gain from them. It extends to stock trading, mutual funds, hedge funds, private wealth, investor management, etc. And includes all means that result in value accretion and optimisation of returns on investment. It is a process/system broken into three phases. And they complement each other as noted below.

1) Front Office - set up trade policy, client/market facing, initiate deal agreements, set up deal/term sheets, conduct market research, and analyse economic outlook. Includes sales teams, trading desks, market research/analysts, portfolio managers, etc. This is where you have the traders, the guns and the money. Rightly or wrongly, people here are thought to arrogant, brash and think they own the world. They are more focused on making money than actual risk management; and think that without them there’s no business. They have a tendency of being absorbed by intense desire to make money that they often forget about the REAL impact of the risks they take. That’s the general thinking but the jury is still out on that. Whatever your view is, they need to be tamed by the Controllers.

2) Middle Office - The Control Function - product control, financial control (aka Engine Room or Know All team), valuation, quant, risk management, regulatory reporting, compliance, etc. These guys control/limit the activities of Front Office guys who are often seen as loose cannons.

These guys don't fully appreciate their role sometimes. And that’s cos they tend to suck up to the Front Office. As a result, rules get bent, slackened, ignored and suddenly you end up with credit crunch. If these guys had done their jobs to the letter, we wouldn’t have had the global financial meltdown in 2007-08.

The crisis actually started in 2006 when there were massive hits against p&l, trading started to slow down and we started hearing of recruitment freeze.

On two occasions I had to block two large trades; but that didn't go down well with many cos of the lost fees they had “locked in”, said @ehokoli. He blocked a trade in 2005 because his Portfolio Manager over traded and had breached his single obligor as well as FX trading limits. The second time was about 1.5 years later when he refused to sign off a deal that would have netted a large fee probably in the region of USD 5m. All hell broke loose. But he was able to demonstrate that the bank was exposed to at least USD 10b loss due to a flaw in a formula (a bug in the algorithm if you may) embedded in the deal agreement, which everyone overlooked. That level of exposure was too high to take on a single trade and was in breach of agreed risk limits.

Controllers are meant to spot these loopholes and “control them” to prevent avoidable operational risks like the UBS rogue trader Kweku Adoboli jailed in 2012 for fraud over £1.4bn UBS loss. Remember that UBS lost about £40bn in 2008 as a result of the financial crisis.

Generally, the accounts and reports did not make much sense back then. Well, they were kind of okay but explanations were watery; full of jargons like the Greeks (delta, vega, theta, gamma, lambda, Rho, etc.) that most people didn’t really understand well enough but either thought, or pretended they did. This resulted in failure of control systems.

But not just control systems. The models that predicted asset prices were flawed. The algorithms also contained wild assumptions. In the 1990's David X, Li came up a Gaussian copula model to calculate correlation between multiple variables. The use of this model was technically abused because it was limited in scope and dimension. It was applied to a period that was comparatively stable, when asset prices consisting mainly of mortgage backed CDO's were upwardly mobile and the CDS prices used in calculating correlation were relatively new. Available sample data was not varied enough. The quants guys were too focused on number crunching rather than the reality on ground.

And the reality was that they used stats from a period when property investment was on the up and defaults were comparatively low or non-existent, to predict the probability of credit default. But the financial time bomb was about to explode. The people that should have seen it coming didn't until it was too late.

At that time properties were grossly overpriced and affordability of mortgage wasn't really tested. The sales guys focused on the commissions they would make rather that the actual risk exposure - ability of borrower to pay back mortgage loans and the real risk of default. There was no experience of, hence no provision was made for unpredictable events such as sudden massive credit defaults that could force a collapse of the financial system, which thrives on credit and trust. The financial crisis was inevitable.

As a way of managing their exposures, Hedge Funds, IBs, Global Asset Managers and Investment Management firms that were exposed started isolating subprime securities (mainly MBS’s and ABS’s, CDO's and associated bonds and derivatives) into silos from which Flow/Proprietary Trading and other risk reduction transactions were executed. Of course it was all too much, too late. Time had run out.

As many firms over-traded, others stopped lending or extending credit. Too many defaulted at the same time, asset pricing models failed totally because the unpredicted “known unknown” happened. Systemic defaults increased astronomically, trust “left the building” and access to credit became tighter. It was the credit crunch. The financial system crashed, banks went bust, people lost their jobs, some traders jumped off skyscrapers in Canary Wharf London, many companies went into administration; and boom! It was the global financial meltdown and the world went into economic recession.

What trumps it all is that many countries are still in recession and country risks are still sky high in places. Everyone appears to keep mum about the prevailing economic/securities time bombs in countries like Greece, Spain and Italy. Will there be another one? Where will it start from and when? Watch this space!

3) Back office - This is the Operations (Ops) Function - IT functions/systems, operational risk control, settlements, make payments based on term sheets, collect and transfer trade certificates, registration with clearing houses, legal and custodial services, etc. They do all the paperwork and make sure that everything is in place.

Never lose power on your smartphone or tablet. Power up with HG solar power bank charger for mobile gadgets.